This post was originally published on this site.

WASHINGTON, USA – The G-24 expresses its deep concern about multiple political crises and conflicts around the world, and we deeply regret the tragic loss of innocent lives. The war in the Middle East is causing deterioration in the well-being of affected populations, as well as damage to civilian infrastructure.

These unfortunate events have taken a significant toll on an already weak global economy, with particularly devastating effects on emerging market and developing countries. We underscore the importance of upholding a rules-based international system, grounded in respect for national sovereignty and the principles of the UN Charter. In view of the profound human and material costs associated with the conflicts across multiple theaters, we call for concerted international efforts toward cessation and avoidance of violence; de-escalation, recovery and reconstruction.

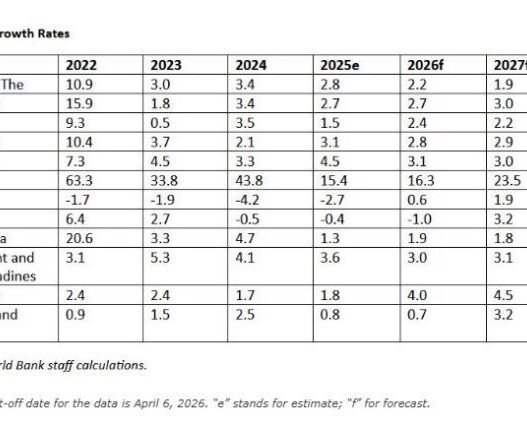

Following a period of tepid but resilient growth, global economic conditions are deteriorating sharply, driven by disruptions to global supply chains, including energy markets, in the wake of the ongoing war in the Middle East. Global growth is now projected to decline in 2026, relative to 2025. If the disruption is sustained, core and non-core inflation could increase, driven by higher energy, food, and fertiliser prices, as well as rising supply chain costs. The G‑24, therefore, highlights the critical importance of safeguarding international maritime routes.

We urge the cessation of attacks on energy infrastructure, given that the restoration of damaged assets to full capacity is both costly and time-consuming. Such disruptions adversely impact overall energy supply and contribute to increased market volatility. The G-24 notes the initiative taken by the OPEC Declaration of Cooperation (DoC) countries to ensure the continued availability of oil supplies, particularly through the use of alternative export routes, which have contributed to reducing oil price volatility.

Given these conditions, the medium‑term outlook for global growth remains uncertain, marked by significant headwinds and increased pressure on the current accounts of oil-importing countries. Inflationary pressures could spill over into a wide range of economic activities, eroding part of the recent progress on disinflation.

Potentially rising interest rates and exchange rate pressures may further increase borrowing costs, exacerbating existing vulnerabilities and complicating economic management in Emerging Market and Developing Economies (EMDEs). At the same time, tighter financial conditions—combined with heightened risk aversion in capital markets—could reduce private capital flows to these economies. This environment, therefore, calls for heightened vigilance from policymakers. While domestic policy measures focused on fiscal and monetary stability, are critical to strengthening resilience and preserving macroeconomic stability, traditional approaches such as contracting domestic demand or allowing currency depreciation may prove insufficient for absorbing the shocks and addressing the challenges posed by deteriorating external conditions. In this context, multilateral approaches, support and increased development assistance remain vital for vulnerable countries.

The need for a strong Global Financial Safety Net, with an adequately resourced and quota-based International Monetary Fund (IMF) at its center, is now more important than ever for safeguarding international monetary stability.

To strengthen IMF’s capital base, we call on members to advance the timely completion of the 16th General Review of Quotas (GRQ). We welcome the agreement on the Diriyah Guiding Principles for Quota and Governance Reforms, which represents an important milestone in the Fund’s governance reform agenda. We call for timely and meaningful progress in the ongoing work on the 17th GRQ, consistent with the Diriyah Guiding Principles.

We strongly believe that the fundamental goal of quota reform must be to enhance the voice and representation of all EMDEs, while ensuring that the quota shares adequately reflect changes in the relative economic weights in the global economy. At the same time, the quota shares of the poorest members must be protected.

During this period, it is essential that the IMF remain a trusted advisor, focusing on the whole range of macroeconomic and macro-critical challenges faced by its membership, and adapting its advice and lending toolkit to serve their diverse needs.

Given the scale and breadth of the impact of the conflict, we welcome the emphasis on the Fund’s readiness to deploy all its tools to assist the membership. In the current uncertain environment, the Fund must remain proactive and agile through vigilant monitoring, timely spillover assessments, and robust scenario analysis. In that regard, we call on the Fund to be flexible in the program engagement—with well-timed program recalibration or adjustments as needed. In this regard, we look forward to the outcomes of the review of the Low-Income Countries Debt Sustainability Framework (LIC-DSF), Financial Sector Assessment Program, and Program Design and Conditionality Reviews. Regarding the Comprehensive Surveillance Review, we reiterate that effective surveillance is one of the IMF’s most important functions. Accordingly, rigorous and even-handed surveillance should be applied to all members.

We call for an early review of the charges and surcharges policy, the Resilience and Sustainability Trust, and the Catastrophe Containment and Relief Trust, all critical to supporting EMDEs. We highlight the importance of strengthening precautionary instruments and reiterate our past call on IMF to explore a mechanism for the regular issuance of SDRs to more effectively support all EMDEs. We welcome the progress made in securing financing assurances to provide additional Poverty Reduction and Growth Trust subsidy resources, and we urge countries that have not delivered yet on financing assurances for the implementation of the General Resources Account distribution framework approved under the 2024 reforms to do so promptly.

The World Bank Group’s (WBG) ongoing focus on accelerated job creation, job‑intensive sectors, infrastructure, and innovative financing is crucial to the achievement of its mission of a world free of poverty on a livable planet.

We recognise ongoing work to address the unique challenges and needs of fragile and conflict-affected states through differentiated approaches; and we welcome the recognition of industrial policy as a legitimate policy tool for developing countries. Adequate financing remains critical for the achievement of these and other goals, and the bank should use the strength of its balance sheet, to the fullest extent possible, to boost lending capacity while carefully balancing increased risk tolerance with the preservation of its financial sustainability and credit rating.

In this regard, we call for faster progress in ongoing initiatives, including the Framework for Financial Incentives, hybrid capital, and portfolio guarantees, all of which are critical to mobilising additional lending capacity at affordable cost. Collaboration with multilateral, regional, national banks and domestic nonbanking financial institutions could focus on mobilising private sector investment, deepening domestic capital markets, de-risking private investment, mitigating currency risks, and increasing access to credit for Micro, Small, and Medium Enterprises.

We reaffirm the importance of the 2025 Shareholding Review to strengthen the legitimacy and good governance of the WBG as a multilateral institution. We reiterate the Lima Principles and the dynamic formula, and welcome the discussion on the issue of unallocated shares after the deadline for the current capital subscriptions for the 2018 IBRD and IFC General Capital Increase and Selective Capital Increase expires on 16 April 2026. We look forward to progress on the outstanding items, including unallocated shares, implementation of measures to enhance voice and representations of developing countries, and preparations for the 2030 Shareholding Review ahead of the 2026 Annual Meetings in Bangkok.

Continued support for developing countries in managing worsening debt vulnerabilities and avoiding a debt crisis that retards development progress is crucial. We welcome progress in the implementation of the G20 Common Framework (CF) for Debt Treatments beyond the Debt Service Suspension Initiative, as well as the Global Sovereign Debt Roundtable aimed at building common understanding on debt sustainability and debt restructuring challenges. We look forward to predictable, timely, orderly, and coordinated sovereign debt treatments, with participation of private creditors, and call for additional reforms to the international debt architecture to promote sustainable debt management practices, enhance debt transparency, and improve country-risk assessments by credit rating agencies.

We encourage the IMF and the WBG to provide support to strengthen the capacity of countries to undertake debt management. Enhanced debt management frameworks, including transparency of debtor and creditor countries, as well as strengthened reporting standards and debt data compilation are key. We call for institutional mechanisms for crisis prevention and response to support vulnerable countries with sustainable debt positions that face short-term liquidity shocks, including through gold sales to bolster IMF capacity and closer coordination between the IMF and Regional Financing Arrangements.

Recognising the varying national circumstances, commitment to accelerate implementation, and cooperation to address the impact of climate change should not diminish and should continue to be guided by the principles of equity and common but differentiated responsibilities and respective capabilities, as enshrined in the United Nations Framework Convention on Climate Change and its Paris Agreement. Tackling emissions from all sources is essential, but it also needs major investment in sustainable infrastructure, mitigation, adaptation, loss and damage, and protection and restoration of biodiversity.

All of these will require scaled-up, sustained and affordable long-term financing, especially grant financing, technology transfer, and enhanced technical assistance from developed countries to developing countries. We encourage the use of country platforms to support energy transition pathways and emphasise the need for greater technical support from IFIs and other Development Partners to mobilise greater amounts of grants and more affordable and concessional climate finance. We urge donors to honour existing pledges aligned to the New Collective Quantified Goal of $300 billion per year by 2035.

Multilateral cooperation is crucial for mobilising domestic resources to finance sustainable development. A key aspect of this is the reform of international tax rules and practices such as profit shifting and illicit financial flows, which deprive developing countries of much-needed revenue. We note the progress on the United Nations Framework Convention on International Tax Cooperation and the OECD Inclusive Framework and look forward to a solution that delivers meaningful and sustainable revenues for countries, particularly EMDEs. We urge donors to reverse the trend of declining Official Development Assistance (ODA) and to honor their commitments and increase their support in light of rising needs. Additionally, we call on the IMF and World Bank to continue providing support to EMDEs through capacity development and technical assistance, ensuring institutions are equipped to implement and benefit from new frameworks.

We acknowledge that unilateral trade actions – including tariffs, sanctions, secondary sanctions, nontariff barriers, and other protectionist policies, especially those that are inconsistent with World Trade Organization (WTO) rules – have extraterritorial impacts that hinder global trade and integration.

To restore confidence and strengthen the outlook for global growth, we call for a rules-based, non-discriminatory, fair, open, inclusive, equitable, sustainable, and transparent multilateral trading system. Enhanced cooperation among multilateral institutions and member-states to promote a consistent and coordinated approach to multilateralism is crucial. As a fair, transparent, and rules-based multilateral system is central to global prosperity, peace, and stability, closer collaboration among the Bretton Woods institutions, WTO, national governments and regional and multilateral organisations will be critical for safeguarding stability and restoring confidence in the international system. To ensure that diverse voices are heard, inclusive membership of multilateral governance and agenda-setting bodies like the G20 remains paramount.

The post Intergovernmental Group of Twenty-Four on International Monetary Affairs and Development appeared first on Caribbean News Global.